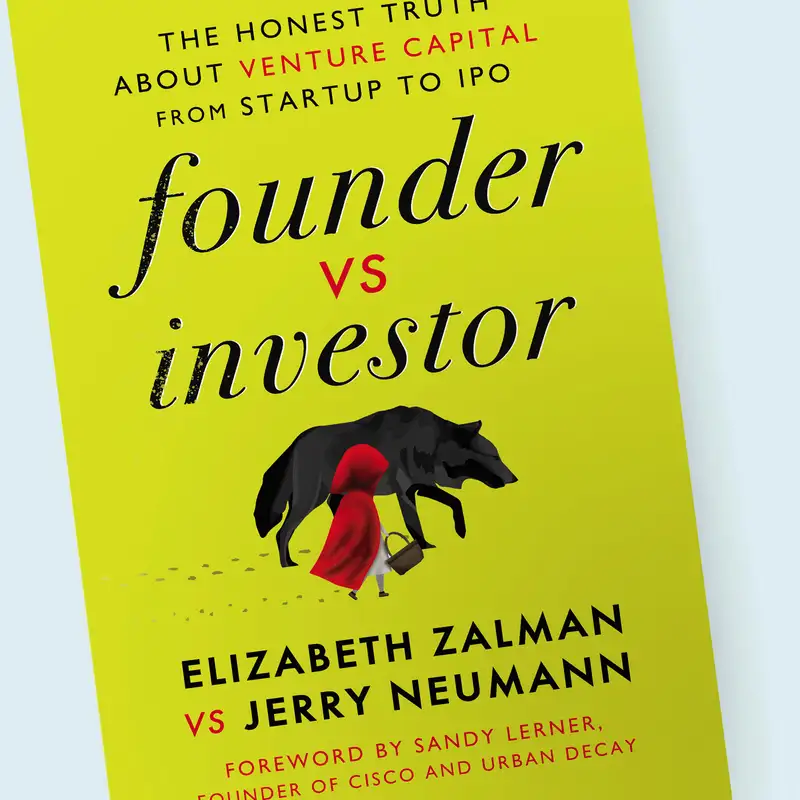

Founder vs. Investor with Liz Zalman and Jerry Neumann

And here he is, the man, the myth, the legend. Bryant, I've got everyone. Everyone is here waiting for you and Steve. No.

Bryan Cantrill:You know what? Just wanted to keep everyone just a little bit late. Actually Hello? See, ironically, of my real pet peeves about VCs that are late.

Steve Tuck:Good place to start. A good place to

Bryan Cantrill:start. Exactly. I would like to point out that we we still made it within the minute. I would like to believe. We wait according to my clock, we were in it at noon and like twenty seconds, but I don't know that day.

Bryan Cantrill:Everyone here, it's great. We've Liz, welcome first of all. It's great to have you here. And Jerry, welcome back. Seth, welcome.

Bryan Cantrill:It's great to it's great to have all three of you.

Jerry Neumann:Thanks. It's fun to be here.

Liz Zalman:Thank you.

Seth Winterroth:Good to be here.

Bryan Cantrill:Alright. I I'm I'm excited for this. Maybe I I I would like to believe that all of us are excited and maybe everyone's like a just a little bit nervous. Or just excited. Or just excited.

Bryan Cantrill:I I don't know. Maybe I I think the reason a little bit nervous is because I think we wanna go into some of the things that are not exposed in this founder and investor relationship and founder and investor behavior. I think we wanna get into some I think we wanna get into some bad behavior, but we also wanna get into some good behavior.

Steve Tuck:Why are these things not more exposed?

Bryan Cantrill:Why are these things not more exposed? Well, do we wanna I mean,

Steve Tuck:not Just

Adam Leventhal:to dance around the title.

Bryan Cantrill:Oh, here it comes. Oh, here it comes. Mister, introduce the subject now. Right. Go ahead.

Bryan Cantrill:Right.

Adam Leventhal:Would the senator from provide some context, please yield?

Bryan Cantrill:Yeah. Yeah. Yeah. Go ahead. Let's do it your way.

Bryan Cantrill:Let's let's

Adam Leventhal:Liz and Jerry have written this terrific book called founder versus investor, where a founder and investor are talking about their different perspectives on very similar material. And so as a bunch of founders and and and joined by Oxide investor, Seth, I thought it'd be good to talk about. So there you go. Context. Sorry, everybody.

Bryan Cantrill:Alright. Well, yeah. Exactly. And also, like, to do this at, like, we're only, like, two minutes in. So we're really Yeah.

Steve Tuck:Can't get that time back.

Bryan Cantrill:Yeah. Exactly. Right. But, yeah, Liz and Jerry, welcome. And Seth as well.

Bryan Cantrill:So let me actually, let's start with Steve. I think your question of like and Liz, maybe you can take a swing at this. You and Jerry in your book talked about a bunch of things that actually aren't talked about. And why aren't they talked about? Why don't we speak more openly about these things?

Liz Zalman:That's a great question to start with. I I think it's because nobody ever really walks around talking about the worst the worst possible things that could happen in their lives. Right? We we go through life and we're like, this is the best possible scenario. Here's the outcome that we expect.

Liz Zalman:We don't go into a date saying that we don't clip our toenails. Wait for the person to find that out when we go to sleep with them. So similarly, I don't think we lead with the bad stuff when we go into a founder and investor relationship.

Bryan Cantrill:Yeah. And you all definitely did talk about a bunch of the things. And Liz in particular, I mean, and I mean, you had in particular, I mean, you there are there are a bunch of like great moments in this book. I loved your sharing is caring section where you're just like, I'm just gonna rattle off all of things that have happened. That was a felt felt cathartic to write some of the stuff down.

Jerry Neumann:You should have seen that section before I asked her to take out some of the stuff.

Bryan Cantrill:Oh, we should see that section.

Steve Tuck:Where is

Bryan Cantrill:that? Yeah. Thank you. This is this is what this is like, who was it that accidentally divulged in the Watergate hearings that there's actually a tape recorder in the white

Steve Tuck:What?

Bryan Cantrill:Now we know it's a subpoena. So, yeah, Liz, tell me about the the origins of that section before before Jerry apparently censored the good stuff.

Liz Zalman:I I think he he correctly asked for a mildly sanitized version. But it is definitely out there. It's look, the book was cathartic. Jerry and I had been through a situation that neither of us were pleased with. And we decided to step back and say, I wonder if we could make this easier for another founder or another investor to get through.

Liz Zalman:And when we got to this part I just let it all go and it was every single nasty little thing that had ever been said to me whether it was related to the fact that I liked to wear a hat on interviews with people all the way through to the things that female VCs have said to me or just awful sort of misogynist or inappropriate things that male VCs said to me. And it was was nice to put them into print in a way that wasn't gonna get me sued.

Bryan Cantrill:So the hat one was on the you may have inadvertently mentioned the hat one because that was Jerry, is that one that you had her cut? It's like, listen. So we the the hat thing, you and I have talked about this before. Can't wear hats with VCs. I just can't

Jerry Neumann:mention that. I had wouldn't have bothered me. No. I don't remember the hat one, actually.

Bryan Cantrill:Yeah. I would I and now I've got a lot I actually got a lot of hat related questions. What what what kind of hat actually for you know, not not that I'm withholding judgment. But

Liz Zalman:I'm a big fan of trucker hats and yeah. No. There's I don't know if you know the brand Goren Brothers, but they came out with those line of trucker hats called Animal Farm a few years ago. And the one that I picked for myself was a picture of a lion and it says king on it. And so it's possible that rubbed people the

Jerry Neumann:wrong way.

Steve Tuck:That's you know what? Great alpha move.

Bryan Cantrill:It is a great alpha move. Yeah. I think, Steve, you and I are both too cowardly. You have worn Cowardly lion. Yeah.

Bryan Cantrill:Exactly. We would I did Liz, total respect for wearing the king hat. I also love the VC's like, hey, next time, like, I don't know. It's the king hat. What had oh, we had us all cowering.

Steve Tuck:There are other choices.

Bryan Cantrill:Right. Okay. So one of the things There are

Jerry Neumann:other choices.

Liz Zalman:Oh, sorry. Go on this.

Bryan Cantrill:No. No. Go ahead.

Liz Zalman:No. No. There are definitely other other other choices. There's a rooster, and it says cock on it. I declined to wear that one.

Steve Tuck:That's what I'm here for.

Bryan Cantrill:That that yeah. That is great. And then what what are the ones that that I actually do want to circle? Because I think that and and maybe maybe it's wrong to start with this as the epicenter, but Liz I gotta believe that this is part of really what informed the book. You had a I mean that it your your lead bullet there is that you had a term sheet was pulled three days before closing.

Bryan Cantrill:And boy, do we feel that one. So could you first of all elaborate on our listeners, what is a term sheet? What does it mean to have a signed term sheet? What is closing? What does it mean?

Bryan Cantrill:Like why is that so I mean, that to any founder is a horror story. So and I I gotta believe that that experience is one of the most scarring that you endured because it cuts against a lot of the social contract that we have between founders and investors. So I wondered if you might elaborate on that in particular.

Liz Zalman:Absolutely. So a term sheet is a piece of paper that an investor gives to a founder. And it says under these set of circumstances for this amount of money under these terms, I am going to invest money in your company. And you, the founder, are going to give me back equity. And we are going to go into business together.

Liz Zalman:And if you're lucky, you get one term sheet. And if you're really, really lucky, you can get two or three or five. And then once that term sheet is negotiated through with lawyers and signed, for better or for worse that that is the future. And everybody wants to work towards a close. And a close is an investor ultimately wiring you money in the amount that you agreed upon for equity.

Liz Zalman:In this particular case, in this instance, I was working with a very young VC, a first time VC, a female actually. And we were arguing over some of the mechanics of how the wires should go. There were lots of wires happening. And this VC was going to be buying out a lot of my earlier investors. So cleaning up the cap table, cashing them out.

Liz Zalman:Okay.

Bryan Cantrill:Interesting.

Liz Zalman:And we got caught up. Yeah. We got caught up in the decimal points of the mechanics of that actually. We were arguing over two versus four significant digits.

Bryan Cantrill:Wow.

Liz Zalman:And in the it was crazy and in the end the VC and the CFO on the other side got so frustrated that they just decided to walk away.

Bryan Cantrill:That's that's insane. I mean, that it but they because that obviously left you in was this was this a lead investor? If you don't mind me asking, was this was this follow on capital? I mean, not that it matters.

Steve Tuck:It must've

Bryan Cantrill:an elite because it's the the sun walking away from the term sheet.

Seth Winterroth:Yeah. They've been a lead.

Liz Zalman:It was 100% elite investor. And it was yeah. It it was surprising that that person's reaction was not, hey. I wonder why two versus four digits is important. But their reaction was, we are just going to walk.

Liz Zalman:And my investors were completely perplexed. They actually placed a call to her boss, one of the managing directors of the firm. And he was just like, well, it is what it is. And I remember what this woman said

Bryan Cantrill:It is what it is.

Liz Zalman:It is what it is. And I went to this woman. I said, you've got to be kidding me. Do you see where this leaves us? And she goes, well, I would be happy to call the other investors that you were fundraising from and tell them that you're still a good deal and they should invest in you.

Liz Zalman:It was

Steve Tuck:Oh, no. Oh, oh, yeah. Yeah.

Bryan Cantrill:I'm to. I'm to. Wait. Yeah. Yeah.

Bryan Cantrill:Absolutely not. That is thank you for for elucidating the things that we will not do.

Adam Leventhal:It's like having your ex give a recommendation.

Steve Tuck:Exactly. Liz, am I remembering correctly? Was this the anecdote where you, I think, one of your investors reached out, but only one when this happened? And you were like, I mean, I'm glad that one person had my back or tried to represent, like, stick up

Bryan Cantrill:for for me in the

Liz Zalman:Yes. One one person reached out. I can name him if you would like. It was James Hardiman of Data Collective. And he called me and he goes, I'm going to ask you how you're doing.

Liz Zalman:But first, do you and the company need any money? It was an amazing phone call.

Steve Tuck:Wow.

Liz Zalman:Yeah. Because he was just like my fiduciary responsibility is to make sure you guys are not fucked over. And then now I'm gonna ask as your friend, how are you doing? It was a God, it's been helpful. Phone call in the middle.

Liz Zalman:Yeah. It was amazing.

Bryan Cantrill:Oh, that is amazing.

Seth Winterroth:That's very that's very on brand for James.

Bryan Cantrill:Hey. Good on you, James. Seriously. Yeah. I I actually don't know James at all, but I'm I'm glad that we called out.

Steve Tuck:Part of this, we started with, like, why don't people talk more about the bad and also but also the good. The good. Because I because I think there and and one of the things that it feels like is there just aren't there isn't the right incentive structure to talk more about this stuff.

Bryan Cantrill:Well, it also I think that because really to to to give James the praise that that he's due, you've gotta You gotta talk about the bad. You gotta talk about the bad. Yeah. You gotta talk about and you don't even you don't need to name the other investor, but you talk about the fact that like this investor walked away from a signed term sheet and three days before closing. And I I think that the first responsibility of venture capital should not do damage in companies they don't invest in.

Bryan Cantrill:Like that it just feels like feels like this is extremely basic. Oh, but I mean, Liz, that's what was happening to you. This VC was doing damage in a company that she was not investing in. Oh, one question for you. Do you feel that this issue was reflected a a lack of conviction?

Bryan Cantrill:Was this a deal that the firm regretted that they had entered into and they were looking for an excuse out? Because it's I mean, it just feels so I mean, what and I'm sure you were trying to think about all these things, like why is this person leaving this agreement?

Liz Zalman:That's a that's a great question. And one I haven't pondered actually. It is entirely possible. I I don't I don't believe it. What what I think ended up happening, and and I'll I'll take some of the blame for this as as I should as CEO.

Liz Zalman:I think I was getting wrapped up in the mechanics, and I also wasn't able to take a step back and say, I wonder why it's starting to become tension filled. And maybe I should ask for some help perhaps for my current lead. But I was surprised in any case that the MD of this firm and maybe even my current lead couldn't get together and find a way to work things out. Because again, and to your point, we, the company, were going to be left injured, like in a really, really bad state. I can't just start up a fundraiser again, I got to wait six or twelve months to do that.

Liz Zalman:And she and her firm were gonna get to walk away completely clean. It was as no skin off their back.

Bryan Cantrill:And they walk away anonymous. They walk away with without seemingly without consequence. And this is what the real frustrating asymmetries that exists in a I think and obviously Seth and Jerry, I wanna get your perspective on this as well because a frustrating asymmetry that exists is it feels like founders is never in your interest to talk about the bad behavior of investors. And you're just trying to like, I'm just trying to live. And the whereas they I think that when you got bad behavior from a founder often tends to be be I think more public although I want I definitely want your perspective on that.

Bryan Cantrill:I I am definitely curious that he from a founder can destroy a VC firm in which they do not take invest. I'm like does the opposite exist? I know I don't think so but I love your take on that. I think that that there is this real asymmetry. And I think that that part of what makes this really that it feels like this stuff does get called out because it's not in the founder's interest to do so.

Bryan Cantrill:But the and so actually let me ask ask this directly. Jerry, in your experience, I mean, sounds like you went through this with were you on the cap table when this happened or this?

Jerry Neumann:I was. Yeah. I I do think there was something else going on here. I mean

Bryan Cantrill:Yeah. I just think. And I it unprecedented?

Jerry Neumann:On people pulling term sheets? No. I I mean, I've pulled term sheets. I but, you know, the the way the reason you pull so what happens before the term sheet is the founder tells you what the company's doing, how they're doing, what's going on. They give you all this information.

Jerry Neumann:You say, great, based on that information, I'm going give you a term sheet. And then you give them the term sheet, then you do some due diligence. They give you the actual documents. They let you inside the company to look and see what's happening. If they lied to you, you pull the term sheet, right?

Jerry Neumann:In this case, nobody lied So to anybody, this was completely different. It's perfectly fine to pull a term sheet if what they told you wasn't true, but that wasn't the case here. So I think there was something else going on here. I personally believe, you know, a lot of people, younger VCs who go work for more established firms have much more downside than upside in doing a deal. So, they could do a bad deal, and then they get fired, or they do a good deal, and unless it's a great deal, it's just a deal.

Jerry Neumann:So, I think some people just can't pull the trigger because they're scared of making a mistake. And this is the kind of thing that kills VCs. Mean, can't be scared of making a mistake because most of what you do as a VC is a mistake, right? Like, know, most of the companies you invest in don't become big. I personally think she just the only way

Seth Winterroth:to see career advancing upside is to do something that by nature is contrarian and requires courage. Yeah. But

Jerry Neumann:some new VCs, when they're new, they get hired, the people don't know if they have the courage or not. If they don't, they won't last long. And I don't think this one lasted long in that firm, if I remember Liz. I think she left soon after, right?

Liz Zalman:Yeah, she got shoved out and put in as the head of one of their companies and I think it slowly shut down.

Jerry Neumann:Yeah. Oh. I blame this on on her.

Bryan Cantrill:List follows the this person's career particularly closely. I'd be clicking reload on LinkedIn every day. I'd be like, oh, fired from another CEO position. What's next? Interesting.

Jerry Neumann:Oh, I take this stuff personally, right? So I actually went on Twitter and called out the firm, which nobody ever does. And I'm like, you know, people should do this. When firms act badly, people should know. But I think I'm the only VC that does that.

Steve Tuck:God bless you. It has certainly

Jerry Neumann:not made me any friends.

Bryan Cantrill:Well, so in that spirit, so we are not gonna name a firm, but we So Liz, one thing you should know about Oxide is we we've had the same experience. So we had from walk away for all we had our lead walk away from assigned term sheet for our series a. And the firm had and maybe this has happened in your case as well and this is why there's just particularly grading this firm had preempted. So we weren't raising, they preempted, they we got to a signed term sheet and then they walked away over the putatively over the we had follow. So they did they did not like one of the investors that we got to follow.

Bryan Cantrill:And we're not gonna name them either, but suffice it to say if we named them, you'd be like, what?

Jerry Neumann:Well, so wait, let me let me ask you a question. So, you know, you started this conversation saying, why don't people talk about these things? Why won't you name them?

Bryan Cantrill:Yeah. I mean, it

Jerry Neumann:would do everybody listening a favor, right?

Bryan Cantrill:We won't name the firm because I don't wanna damage their portfolio companies. I don't wanna damage their portco. And but that said, like I think that there should absolutely be consequences for it. And I I'm hoping we get Seth to expand on this a little bit because Seth was Seth was heroic in all of this. The end of Eclipse was heroic in all this.

Bryan Cantrill:But so they and again, they they backed out because putatively because they objected to the follow on capital. Actually because the mark it was 2022 and it was a bad market for venture in 2022. And they they didn't like the fact that they had gotten over the line. They were they were having regret. And in particular, they tried to reprice us, which is just unconscionable.

Steve Tuck:What would that mean? That that's just a a way of trying to get out of the deal. I mean, that would that was merely to get to an an end that was they wanted to back out. And I I think one thing that was I mean, first of all, just to to wind back, like, fascinating book that any founder and any investor, every founder and every investor should should read. And I first came across it by way of invest like the best.

Steve Tuck:So great podcast, and and you two were on there, and it was more contentious in podcast format than it ended up being in the book. And the book ended up being just like such an amazing long form of going to depth on the the unique incentives and and and some of the constraints on being a venture capitalist, and then the same on being a founder. And I think as as Brian and I talked about a lot, like, was amazing how much you both agreed on, which may be an indictment on the on of the VC community and then the founder community. But the in in this particular case, this one of the things we found ourselves spending a bunch of time on is trying to understand partnership dynamics. Yeah.

Steve Tuck:Yeah. Because you you'll have a partner who is very spun up on a company. And I mean, Liz, you you've definitely hit on this a bunch, but this only gets over the line. A fundraise only happens when a partnership is in agreement. Most firms are consensus driven and and require that you have got consensus in the firm.

Steve Tuck:And in this particular case, you had a partner who was very excited about the deal and kind of, like, rapidly grab or, you know, grabbed this tepid partnership over the line only to feel more and more pressure probably between term sheet and what would have been closed and resistance. And they inevitably caved to the pressure inside the firm and backed out. Backed out.

Bryan Cantrill:A foolishly sent us an email explaining that they were backing out because of the investor in the syndicate. Like, I mean, I guess, like, you guys are so incompetent because Jerry, to your point, they could have done much more damage to the company if they're like, oh, we discovered something in diligence that we can't even talk about. That's just too horrific to mention. That would have been really bad. But they did I guess they didn't do that.

Bryan Cantrill:And What was good

Steve Tuck:is they said, we don't like this really good investor.

Bryan Cantrill:This good investor whose feelings were really hurt, by the way. They were they were like, we've co invested with them in a lot of deals. Always thought we were really like, we were we don't have sharp elbows. We thought we're like, Nate, it's not you. It's not you.

Bryan Cantrill:It's the lack of conviction. Jerry, I will say this. The so in in terms of again, we would we we name them in private and we And were I'm not trying to put you on

Jerry Neumann:the spot, I'm just trying to point out, like, the reason people don't talk about this stuff is because everything's interconnected, right? So, talk about it, this whole book came about because after this problem that Liz had with one of her existing investors, I was just pissed off. I wrote a blog post called Your Board of Directors is probably gonna fire you, which hit like the top of Hacker News, and Liz called me, she's like, Is this about me? I'm like, Yep. And she's

Seth Winterroth:Why don't people write this stuff?

Jerry Neumann:Why didn't you tell me this beforehand? I'm like, Well, you know, I did. This is actually an email I send to founders. It was I actually think the blog post was really like balanced, and it was I think it was I I stand by it. But I got a lot of emails from VCs being like, dude, you can't say that.

Jerry Neumann:You can't tell people this stuff, because then they're not gonna trust us, they're gonna treat us differently, it's not gonna work. And I was like, you know, if you want it to work, then make it work. It works for me. So I don't know. I think just speaking out can sometimes be a problem, because people don't want to change the status quo.

Jerry Neumann:And so Liz and I decided, like, we're like, You know what? We've got nothing to lose, which of course is never true. Let's write this book as if we, you know, and just tell people what we think. It's not so bad, but we didn't wanna go in and just agree with each other like everybody always pretends to do. We, you know, we want to tell people what it was really like.

Bryan Cantrill:Well, I think as Steve says, did people an enormous service by doing that. And I would say the other thing I would say in terms of and I you know, there was clearly ultimately consequence for the VC that walked away from your signed term sheet. I will I will say one thing that one of the the any interesting moments along the journey, we were talking to another another investor actually looking at our B I think at that at that point. And we were retelling the story. And VC is like, wait a minute, can I guess the firm?

Bryan Cantrill:Like you guys haven't named the firm, but if I guess the firm correctly, will you let me know? And Steve and I like, obviously we're gonna name the firm anyway. So yeah, of course we're happy to let you guess. And one of the other partners had gone to the bathroom while we were talking to her. And she had a guess that was incorrect.

Bryan Cantrill:And then she had a second guess that was correct. And Steve and I did I mean, like, I think I let out the same whoop when the broncos scored the game winning field goal yesterday. I mean, you and I acted like we just seen a buzzer beater.

Steve Tuck:I mean, it was impressive.

Bryan Cantrill:It was impressive. And he came like storming out of the top of like, did I miss? Like, what's going on out here? And he had like, he's like, did someone like make a shot into the trash can from like across the room?

Steve Tuck:Right. And I was like,

Bryan Cantrill:he had a good intuition like, you know, that would also be the kind of thing that would get us all that. But anyway, that was really interesting. And I think it said like, this is not the first time this has happened. And so this is I kind of like get you in on on and then Jerry wanna get back to to to the the points you're raising, but do you want to call out in the in the spirit of calling out James, Seth, when that happened, you all were absolutely heroic because we either the company was left really in the lurch. They had preempted us.

Bryan Cantrill:They had distorted our process. We'd gone around. We'd shopped ourselves on this term sheet. Like we we were in a real pickle and Seth what was your your kind of thought process when that whole thing went down?

Seth Winterroth:Frustrated. It was like a it was that aberration in June 2022 when the market freaked out. Everybody pulled back and then we kind of got back to business within six weeks so you know obviously super frustrating. I think like you know once I'm involved though I'm all in right and I love this company. And I just have so much conviction, had and have so much conviction in what it can be.

Seth Winterroth:And so there was never a moment hesitation for me. And frankly, never a moment hesitation for my partnership either.

Bryan Cantrill:That was the thing to do.

Seth Winterroth:And so, like, listen, you know, I think it's like, there's a lot of bad behavior across the ecosystem but there's a lot of good behavior too and my mindset on this is really whenever there's bad behavior from the venture ecosystem, it's just another opportunity for myself and Eclipse in a business of selling a commodity capital to differentiate ourselves by being full throated in our conviction buying the companies that we work with. And when there's a challenge, that's really the litmus test of a good board and a good set of investors on your cap table. It's easy to be along for the ride when everything's up into the right. You know the whole reason for us to be there as partners and supporters is when there are those types of moments. So for me it was just like hey, it's an opportunity for us to lean in and support these two guys and the wonderful company that they're building.

Seth Winterroth:And boy, has that yielded dividends for us.

Bryan Cantrill:Yeah. And I think that the I mean, so Seth, just to list to you kind of what James did for you, it was very very similar conversation. Like, first of all, like, how are you two? And by the like, let's let's lead this round to the best of our ability, which by the way, we're already tapped out of our I mean, we we're not gonna be able lead very much, so it's gonna but we can at least take over the round, which was huge. Yeah.

Steve Tuck:I mean, it allowed us just

Bryan Cantrill:to It's also just like

Jerry Neumann:a lot of a lot

Seth Winterroth:of capital that wanted to come into the business. Yes. And so it was like a pretty easy you know, it's like not all altruistic either, right? Like, we have a large and existing investment in the business. Like, I still believe deeply in the, you know, the business in the business's potential at the time and there's a lot of capital that wanted to come in at a fair price and to let that kind of stymie going back to like Liz's point in the book.

Seth Winterroth:We would have been kind of back to the starting blocks for six, twelve months. And we weren't in a cash position to go do that. And so it was a good opportunity to go to catalyze interested capital into the business and be able to continue on our journey.

Bryan Cantrill:Yeah. So and actually, Liz, this question for you, how does this informed how you that investors? I mean, do you because I know that, you know, when I look at our process, when we I mean, we got obviously extremely lucky and we definitely did reference checking and so on.

Steve Tuck:Well, I I do wanna point out in in the reference checks on clips Yeah. Specifically, we talked to a couple of their customers. And, I mean, it's kind of like hiring. If someone is providing you references as they are trying to get hired at a company, like, there there is not an incentive structure for people to give negative feedback necessarily, but you will but in this particular case, you know, you had portfolio companies that were, like, just able to give us, like, the real hard truths about their relationships.

Bryan Cantrill:Have we told Seth about these calls? Because I

Steve Tuck:We're doing it now.

Bryan Cantrill:No. But I Seth, one thing you should know is one of these portcos is like, oh, you guys raised a $20,000,000 seed. Wow. Have you thought about just splitting it and running for your lives? And we're like, totally happened.

Bryan Cantrill:Literally joking. I mean, it's like, no. Like, seriously, like, could that's a lot of money. You could actually, like, you could live on the lam for a long time. Like, no.

Bryan Cantrill:You had not thought about that. No.

Steve Tuck:Not doing that. We so talking one of those catch everything

Seth Winterroth:in reference checks. Talking

Steve Tuck:to one of their portfolio companies, he said, look, they are good investors when times are good. And kinda gave some examples of good times. And then said, but they are great investors when times are tough. And then gave some examples of, you know, difficult boardroom situations where you had people with different incentives that were trying to do things that were not in the best long term interest of the company. And that Eclipse has stood up and said, like like, if if you, you know, just double down around the long term vision of the company, and that was super informative and helpful.

Steve Tuck:But I I think where you're going with it is, like, we did not do more than a couple of reference checks. And and and but those definitely checked out. I know, Liz, you you talked about making sure to take time, which is really hard when you are in the, like, rush to get to a term sheet. And then you get these things put on the term sheet, like, oh, this explodes Sunday night at 5PM. You get handed it, you know, Friday at 1PM, and you you feel you can feel panicked, like, I've gotta take this or else.

Steve Tuck:But to actually buy yourself the time to go do proper reference checking and just getting to know the investor better is both hard but super important. It sounds like over time you've gotten you've gotten much more in-depth on that.

Liz Zalman:The mistake that I made in the in the first situation where the term sheet walked is actually an existing investor on my cap table. This woman used to report into him when he ran a a public company. So in my eyes, I was like, oh, she's going to be great. It's great. It's already vetted.

Liz Zalman:And that was an incorrect assumption. Now I actually start vetting before so I create my list and I go through my process. But before I even have an email going out, I am back channeling to various portfolio companies that belong to each of the investors to find out what's going on. And when I ask VCs for references, I also ask for one that is currently contentious so that I can hear how conflict is happening today. And a good VC will say, Okay, here's the situation.

Liz Zalman:Here's what I think they're going to say. Here's what I'm going to say about it. But please go talk to them. So yeah so I've moved that process on up. And then in terms of your point about a term sheet exploding when a term sheet has been issued to a founder I think the number one mistake that founders make is they rush.

Liz Zalman:And in fact that's when the founder has maximum power which is the VC doesn't want to pull the term sheet. The VC really wants to do the deal. They definitely don't want you shopping it. And so a founder can take their time. A founder can be methodical.

Liz Zalman:A founder can think through everything. So long as the founder is working towards a deal in good faith that VC I believe isn't gonna go anywhere.

Steve Tuck:Jerry, can I ask you what because this is something when we were raising our seed Yeah? That we fretted over very, very deeply. We were we were extremely concerned, and people who were in the industry were like, no. No. No.

Steve Tuck:No. No.

Bryan Cantrill:Negotiate that away. Negotiate it away

Steve Tuck:and just say, like, no. We should go to dinner together next week. We just gotta get to know each other because you're what you know? And just for the broader audience, the the reason one might give a term sheet on a Friday and have an exploding clause on, say, Sunday night at 5PM is because firms typically meet as a partnership on Mondays. And if there are other investors that are interested in investing in a company's round, they if they are not already there, will certainly have to have one more partnership meeting to be able to get all the way to a term sheet.

Steve Tuck:And with this clause, if a founder is convinced that it truly could go away Sunday night at 5PM, then what you do is you tell all these other investors, hey, you know, you have until Friday night or Saturday or Sunday to let us know if you guys would like to provide a competitive term sheet. And, you know, most other firms are like, we can't do that. That that that we we would need at least until Monday. So it can put founders in this in this trapped position of of not being able to understand what the other market opportunities are out there. Jerry, why does this Well, clause

Jerry Neumann:doesn't usually. I mean, I've never put one in, but I think it's

Bryan Cantrill:Oh, fair bless

Jerry Neumann:you. I mean, I've never given a term sheet where I didn't know they were gonna say yes already.

Bryan Cantrill:Oh, interesting.

Seth Winterroth:That's a really important point.

Jerry Neumann:Yeah, right? I mean, think this is Seth and I are on the same page here. You can't compete on price. You can't win if you compete on price, right? This is what it's the loser's the winner's curse in auction theory.

Jerry Neumann:If you've got 10 people bidding on a company, the highest bidder has, by definition, overbid. So if you're competing on price, you've already lost. So you need to get in there and convince the founder that you're the right partner, and I mean, hopefully that's because you are the right partner, and then you figure out what the term sheet should look like, you give them the term sheet, and you expect them to say yes. And if they don't say yes, then as an investor, I feel like I've dodged a bullet, because this isn't somebody who wants

Steve Tuck:to partner with me. Interesting.

Seth Winterroth:I think that's right. And like it goes both ways. Right? When I was I was early in my career at Eclipse, a young partner and I tried to preempt a company and the founder said, hey, like that's not those aren't I think I can get a better price essentially from the market.

Jerry Neumann:And it's

Seth Winterroth:like, great. And he went out and fundraised openly in the open market and couldn't get any offers. And came back to me after having run down the runway quite a bit saying, hey, does that deal still stand? I said, okay, yeah, but I'm going go take this through my partnership. But let's shake hands that you're going to take these terms after I go put myself on the line to go do this deal.

Seth Winterroth:He said, yes, yes, of course, of course. I went out, did the work, worked over the weekend, you know, did all the work to get my whole partnership aligned, you know, got approval to do the deal, gave him a term sheet, he went and shopped that term sheet, took a higher offer. Oh. Like this stuff, this stuff happens across the board. I think the mentality there is is that's not the right partnership for me if that's Yeah.

Seth Winterroth:Those are the cards that are gonna be shown. I don't think it makes sense to go like, if we could sit here and talk about all the scenarios where the worst of this ecosystem comes to fruition and I love. Yeah. The book because it helps founders guard themselves against those things and and create leverage and pivotal moments where you can make sure that you're you're protecting yourself and your life's work appropriately. But the but the better thing is to talk about the out upsides and when this stuff goes right, you know, that's the greatness, that's the magic, that's the wonderful aspect of what we do I think Jerry's point around like never giving a term sheet that he didn't know was going to be taken.

Seth Winterroth:That's that's the abundance mentality where you've done the work on the front end with a team that's like Jerry, I'm sure it's a lot of early stage investing, right? So, they've cast their ship into the abyss like failure is almost certain. The odds are so stacked against them and yet they've found somebody, Jerry, who believes in what they're doing, has a unique, you know, perspective, a unique ability to lift the slope of intact, improve of attack, to improve their odds of success, and yeah, like, they've already decided pre pre term sheet to the process that he's run that they're going to go work together and that's the way that I like to run it too. If you're, if you're, like, have a a CRO at a company that says, if you're, if, if you don't know who's going to get the right responder, the the the winning response to the RFP and it's not you. You don't know that you're submitting the term sheet.

Seth Winterroth:It's going to be accepted like, it's not you I feel like that's the right way to approach this early stage investing dynamic.

Jerry Neumann:Yeah, and the other thing as an investor, and sorry to any of the founders or would be founders here, is there are plenty of fish in the sea. If somebody doesn't want to work with you, move on. I mean, you know, seriously, like, you know, every VC says they see a couple thousand deals a year, and that's true. And there's always other deals. So, you know, there's nothing worse than being like, I have to be in this deal, and then it being an awful relationship, especially, you know, and I do, I invest usually first check.

Jerry Neumann:So it's a long relationship. Mean, Liz and I have worked together now for twenty years, I think.

Bryan Cantrill:Yeah. And I think from a from an from a founder perspective, there are many fewer fish in the sea. Because there are especially, you know, when you're, you know, because you're gonna be off thesis for a bunch of I mean, you know, are only so many term firms where you're gonna be on stage on thesis where there's gonna be a fit. I think that, you know, one of the early pieces of advice that we got that I I know that you and I, Steve, went back to over and over again is don't overly fixate on the economics of the deal. That all these other aspects way more important and it's I think Seth this dovetails to what you're saying as well.

Bryan Cantrill:That it's like it's way more important to gear the company to success than it is like you you can get in your own way on the economics. And I I feel that that has been certainly I mean, so when we've always been looking and actually it's funny because, I mean, how many times, Steve, have we been grateful that that firm walked away from that signed term sheet and and the series a because they would they were actually the wrong investors. And we are so much more grateful for our existing cap table.

Steve Tuck:Well, I mean, to the point where when we when we faced, you know, a a a decision that we may have to make, you know, in a couple of days. We we talked about it a bunch. We're like, well, how, you know, how much do we want to buy ourselves some room to close out other conversations, make sure we feel comfortable with with our investor? And, you know, I think we we had the conversation just like this is the right investor. I mean, Jared, to your point, like, we we the the term sheet that was extended was, I think, extended with high confidence, and we took it, and it was the best decision we ever made because we we had a investor that wanted to be a long term investor in in a project that was gonna be measured in a decade plus, not In in a year or two.

Bryan Cantrill:We are in danger of overthinking things. So Jerry, one of the things that we came back to Eclipse with is we were concerned that they were taking advantage of us in the event of Steve's untimely death. And do you remember this? Yes, Steve. There's like and and I remember Leroy being like, Is he ill?

Bryan Cantrill:Does he have some like why would we be talking about Steve dying? Well, no. But just in the event that Steve's dying, it seems like you would have leaving this verbiage and they were just like, what where are we? Where are we right now? Like, what are you guys are free, like you're you're way off the track here.

Bryan Cantrill:Like, yeah, fine. We'll change the verb to like yeah. Can we keep Steve alive? Why are you talking about Steve? So I Seth, I'd like to apologize to both you and and Lior and the firm.

Seth Winterroth:You guys overthink something? Come on. I do like I do like the like Liz said something in the book about, like, valuation. And there was, like, comments in there about, like, partners over price. Think I think it was, like, either these are my words or hers.

Seth Winterroth:Like, price is a can be a rounding error error in like the long term but like integrity you find out like pretty quickly. And I want to go back to like the the moment where your guys' term sheet was pulled because there was a discussion inside my partnership of like okay like should we should we like match these terms or should it be at a lower price? And like what we quickly came to was like to the point you just made, Steve, of like this project is measured in decades, decades, right? The vision for this company is so big. We're going to, you guys are going be working on it for many, many, many years to come.

Seth Winterroth:And at the moment, when like you guys were licking your wounds from having a term sheet pulled, like the discussion literally in our partnership was like, worst possible time for the future for this relationship to go get, you know, a penny wise and pound foolish on price. Totally. I think that mentality has to go both ways though. There's too many cases where founders are optimizing for 10%, 15%, 20% at the series A or the series B when you literally have a decade plus to go to build anything of value.

Bryan Cantrill:Yeah. Totally. Oh, and I and I and hopefully we've hit that balance on our side too, Seth, because I feel with the the same way and have always value it's like, you know, you had a line for me and I can't even remember. I don't think we were talking about me, but we may have been, but you had a line that has really stuck with me about it's gotta be company over ego. Because when you're especially when you're negotiating something, like your own ego can really get in the way and you can just on anything.

Bryan Cantrill:Right? It's just natural for our own kind of our own sense of self to get in the way. And what's like you all of us together have to be thinking about is we are all I mean, the thing that ultimately bonds founder and investor, we are trying to build a successful company together. And all of us have to kind of put the company over the ego, which I Seth, I've I've thought about that a lot.

Seth Winterroth:Yeah. Most great things come from putting the we before the me, which is challenging when like it's your company, right? It's your life's work. And I I I'd be curious actually, Liz, how how you think about founding of a company and board member fiduciary. There's some comments in the book around that type of dynamic.

Seth Winterroth:And certainly the forward from Sandy Lerner kind of speaks to some of these dynamics as well. Be curious how you think about that.

Liz Zalman:Yeah, she's great. She's fantastic. We're so lucky that she agreed to write that. So the exact quote referencing on valuation actually came from Godfrey Sullivan, the former CEO of Splunk, who said, if you do everything right at the end of the day, everything is a rounding error. And that's somebody who's been through it before at multiple companies.

Liz Zalman:And I take that to heart. And so when I started mean, I'm pretty long in the tooth now. I'm on my third venture backed company. But I learn something new on every single fundraise. And so for this company that I started called Sandgarden back in September, valuation was the least of my worries.

Liz Zalman:I was focused on control. I was focused on how co founders would vote together or be unable to vote together to keep control. I was focused on board composition. I was focused on thresholds that the preferred that investors had that would have limited my ability to sell the company quote unquote earlier if I thought it was the best thing for the company. So it was around my ability to control the future of the company as opposed to some future arbitrary value that may or may not ever come to be.

Liz Zalman:And another thing actually that came up with this company was that I insisted on naming board members in particular and actually having control. So if a board member Seth, if you were to die, for example, and your firm had to appoint a new partner to my board, that I would have control over who that partner would be. Because we're in a relationship, and I didn't want a venture capital firm to arbitrarily be able to put a partner in place with whom I had maybe a negative relationship or maybe not the best working one.

Bryan Cantrill:Yeah, interesting. Okay, so on the board, okay, one thing I'm definitely curious about because you I think the times that I laughed out loud at the book is when you talk about you go just open loop on board meetings that are not useful. We've we have I think always been had the luxury at oxide of being having a really honestly useful board in part because I mean Seth, I think you and I and Steve all got a chance to learn from one of the all time great board members in the history of Silicon Valley, Pierre Lamond. One, so I I kind of Liz, one question for you is has have have your feelings about board board meetings moderated at all? And then Seth, I wanna be sure to get to you to talk about how in Jerry maybe what you've seen in terms of how words can be effective.

Bryan Cantrill:Because I do think that like and I think we may we've been spoiled by having just an outrageously good board in that regard. But Liz, have you how what do board meetings look like? Are you have you have you satisfied your life's ambition of the once per year board meeting?

Liz Zalman:Fact, once per year board meeting is indeed codified in my SunGarden doc. Yes. And I assume that that will change on my series a, but I do not have board meetings today. My board meetings consist of me proactively reaching out to people who are experts in a particular area and getting their opinion. So I am still a huge fan of my shadow board, which is people that are good at one thing and exactly one thing and helping me as opposed to these, you know, conscribed quarterly updates where we go through stuff and it's just spinning our wheels.

Seth Winterroth:But the comp the company's at the seed stage right now?

Liz Zalman:Yes. We're at the seed stage.

Seth Winterroth:Yeah. Yeah. Yeah. Mean, that makes sense. Like, what do you do at, like, a seed stage board meeting?

Seth Winterroth:Right? That's that's the kind of like a waste of the founder's time, so to speak.

Bryan Cantrill:You know, I didn't I didn't though know that it was a waste of our time. I always felt like so I here's what I've always felt was very productive about the board meetings even at those those early stages were because you know, Lior had had a line for us that are for me actually that was really interesting. He's like, you know, at Eclipse, the companies that have not been successes, the ones that didn't listen. And it's really important that that and I I thought that was that was interesting. I mean, it was like, okay, I think I I get the message.

Bryan Cantrill:I think who this message is directed at, it would be me. So I got you. But it was also like really important to me, like existentially important that you listen and the And so I think that one board meetings gave a cadence for that. It also just gave us a cadence to have our own like present our own narrative for for where are we? I mean, we we Steve, you and I had always vowed to not do make work for board meetings, which I

Steve Tuck:think we Well, those that we used it to say, you know, let's make sure the information that we have internally for the company in terms of priorities, risks, what's changed, that we use those as a period just a point of organ reorganization or organization to kinda get your thoughts together, and you have to be able to distill it to folks that don't have much as much context and are obviously, you know, going from, you know, a number of different companies and board meetings. So they've gotta be able to, like, page it in quickly and then be able to have, you know, hopefully productive conversation about it. And then and and I think the things that we found valuable is that, you know, Pierre would come in having read the materials cover to cover and would have only a handful of questions. And most of the time, those were material and on point merited discussion.

Bryan Cantrill:So Seth, you obviously got to to, be in a lot of board meetings with this guy and over a bunch of different companies. What is your perspective on how to be a productive board member?

Jerry Neumann:Number one, read the material.

Seth Winterroth:Amazing. I'm on 12 boards right now. It's amazing how many people don't read the material. I think in general,

Bryan Cantrill:like, just the bar is so low when it comes to investors

Seth Winterroth:and VCs. It's like that you are the average of the five people you spend the most time with. Fortunate enough to have a bunch of partners that really aren't VCs in the traditional sense. And I really don't spend a whole lot of time around other VCs because I think the bar is fairly low. Read the material.

Seth Winterroth:I think my comment on the seed stage is most seed stage companies are raising a couple million dollars. They're doing the work to understand what product to build for what subset of customer they're iterating. It's the idea, maze, of getting to a place where you've got a product to deploying or distributing and real traction, that sort of thing. And the plan can change week to week, month to month. And so having a quarterly board meeting, you guys weren't that.

Seth Winterroth:You raised, what, dollars 25,000,000 right out of the gate. You knew exactly what you wanted to go to. You hit the run. You hit the ground running. You know, it was it it was in the meat of it very very quickly and there were some very important decisions across all aspects of the business made, you know, in the first six to twelve months of the startup.

Seth Winterroth:And any one of those things, think like how much of the stack do you want to go develop against? Which partnerships from a component perspective do you bring on? How do you think about what is your process for hiring? There were so many fundamental things that you guys did in the early days that have set the company up for where it is today that if you had gotten those things wrong, we might be telling a different story here. And so those board meetings were pretty meat and potatoes from the jump.

Seth Winterroth:I think Pierre set the bar for me in a lot of ways because he didn't come in and pontificate or be prescriptive. Or at least he most of the time, he didn't. He came in and he was prepared. He asked a couple of good questions. He pushed your guys' thinking.

Seth Winterroth:I think you got a lot out of it. And hopefully, he was able to help you avoid stepping in a pitfall or two along the way.

Bryan Cantrill:Absolutely. Jerry, do you know Pierre? Have you ever have you ever co invested with Pierre?

Jerry Neumann:No. I don't think so. No.

Bryan Cantrill:Pierre Pierre was at Fairchild back in the day. He got a very funny story about hiring Andy Grove at Fairchild and rating Andy Grove's assignment harshly. Andy Grove harboring a resentment about that years and years and years and years later. But Pierre was and then was at with founder of NetSemi and then was or on that kind of that founding team and then was with Don Valenton at Sequoia for many years.

Jerry Neumann:Okay.

Bryan Cantrill:At Coastal and then Klipsch. So he I mean, Pierre has just seen it all. And if you're yeah. If you're doing the math, I think just celebrated his 90. Right, Seth?

Seth Winterroth:Well, I would say anyone who thinks they're long in the tooth when it comes to startups, Pierre's at 95, he's still making angel investments. So we Oh, yeah. All we all have a long way to go.

Bryan Cantrill:And I mean Pierre would always call us like, I mean, he's like, well, listen young man. I'm like, I'm years old. Are we okay. You know what? They're The but I I think that we so yeah.

Bryan Cantrill:Jerry, if you ever Cara was famous for being a diligent board member and really was a template I think for us. But so Jerry, what have you seen in terms of of how boards can be productive from the investor perspective?

Jerry Neumann:So that's not the question I'm going to answer. You know, look, boards are great when your company is doing well. You know, it's the everybody's happy. The board's going to support the founders because it's going great. It's when you hit bumps that the relationship can get contentious, obviously.

Jerry Neumann:I think the thing that founders forget is they work for the board, right? They are employees of the company and work for the board. May think that the company is their baby, but once you take somebody else's money, you work for them. And if you treat your board as partners as opposed to your bosses, then you can get yourself in trouble. So, you know, the email, the blog post that started the book beforehand, basically said, look, you as the CEO, as the founder, you run your board.

Jerry Neumann:You are there to the VCs have to be there, right? That's part of their job. They have to see what the company is doing, it's a fiduciary duty, and they're there to make sure that their investment is going where you told them it was gonna go. They're not there to provide you with help. They will provide you with help, maybe, but that's not really their job, right?

Jerry Neumann:They gave you the money. You do the job. If if they could do your job, they would do it. Right? There's much more money in being a founder than there is in being a VC.

Jerry Neumann:You know, you look at the Forbes 400, how many VCs are in the Forbes 400? It's like, there's a handful. How many people who are entrepreneurs, or children of entrepreneurs, or x y's of entrepreneurs? It's a huge proportion of the list, right? So VCs can't run your company.

Jerry Neumann:If they could run your company, they would go run a company. So you can't expect them to be the ones to help you run your company. They do have good advice sometimes, but they'll give you the advice whether or not they're in the board meeting. Your board meeting should be you telling people what they need to know to do their fiduciary duty. If you want their advice, call them outside the board meeting.

Jerry Neumann:Because once you get further along, and you have later stage VCs in there, people start performing for each other, like the VC is performing for the other VCs, and you don't want to go in there and ask them a question that you don't know the answer to, because they might start to think that maybe you're not the right person to do the job. I mean, you know, Sequoia is famous for having said that they believe that half of the founders they back will be fired and replaced before the company goes public, or gets, you know, exits. And that's, you know, those are Sequoia companies, right? That's probably the low side of that number. You know, you don't want be the founder that gets replaced because you didn't treat your board right.

Jerry Neumann:I just I always found there's a certain naivete among founders, where when I worked for a public company, and I knew the CEO, and I got to see him before and after the board meeting, that's not how he treated his board. Even though he had handpicked his board, and, you know, none of them were major investors, he didn't go in there and be like, so what do you think I should do? Right? He would never ask that question. He would ask that question to people when they're outside of the board meeting.

Jerry Neumann:But in the board meeting, was like, Here's our problem, here's what we think we should do, here are the three of the things that we looked at and discarded, This is what we plan to do, unless you've got a better idea. And he had done more analysis than any of the board members. So they were like, great, you know what you're doing. We trust you to do it. Our full faith is in you.

Jerry Neumann:And that's what you want with a board.

Seth Winterroth:I think that's the right I think like it's management's recommendation to the board. We have a problem, there's a fork in the road. Here's the data that supports either one of these paths that you can take. Management recommends that we should take the left, not the right for the following reasons. Does anyone speak now or forever hold your peace?

Jerry Neumann:Yeah, totally. And the best founders I've worked with, did the ones that, the ones who got in trouble are the ones who walked in and said, We have this problem, I'm open. What do you think I should do? And usually, wasn't quite that blatant, but it was along those lines.

Seth Winterroth:The other trap I see is like Yeah. Like like and we've we've made this mistake in the past, you know, at Eclipse, which is like everyone's a former operator. And so you lean in and try to do too much in these companies. And the reality is like great founders, A, probably don't want that. B, need to build up the internal infrastructure within their own company to be able to problem solve without the need of investors that were former operators stepping into the business.

Seth Winterroth:So what I look for in your guys' board meetings is like very specific acute problems that we can bend the lever in your favor on, Right? Some of this component stuff. Right? Yes. We're thinking through like, hey, this search firm versus that search firm to go retain, you know, in order to go after this leadership position or, hey, we've got a customer that we know maps their use case maps to these two or three other customers.

Seth Winterroth:How can we go get a c suite or a board level intro into those folks? These are high leverage moments where we can bend the odds in your favor, but that's not that's not anybody on the clip side doing the work for you.

Jerry Neumann:And I Seth is right, there's some things that VCs are quite good at, right? And that's like, things like hiring, like raising more money, things that the founders and the operators don't do that often, right? I mean, there's only so many times in your life you hire a CFO. There's only so many times in your life you raise money. VCs see these things much more than founders do.

Jerry Neumann:So bringing them in for that kind of thing is great. I think the other thing to bring VCs in on, and your board in on is, look, they only make money if you make money, or you only make money if they make money, and they want to make money. So, all right, am I going in the right direction to maximize the value of this company? And they can tell you yes or no. Like, you know, that direction, we don't think that's going to maximize value.

Jerry Neumann:This direction, it probably will. And that's high level strategic. It's not like nitty gritty, you know, operational stuff.

Bryan Cantrill:Yeah, actually. And Liz, you had an anecdote in the book about a member of the board that was really former operator, if I recall, and I can't remember if it's you or Jerry's anecdote over that they were former operator that was really, Seth, to your point, like getting two hands on, and they kind of had to be, but not out of malice, they're just like, they were just used to being an operator.

Jerry Neumann:Yeah, that was me. Yeah, he had been the CEO of a company, they brought him on as a operating partner at the firm, because they hope to bring him up to be an investing partner. He was on the board with the investing partner, and every meeting he would just take over and start being like, Okay, but here's what we need to look at. Was as if he was the CEO. It was frustrating because I didn't want to know what he thought.

Jerry Neumann:Like, don't care what he thought because he's not in charge of the company, right? Also not there 20 fourseven like the CEO So, you know, he was working on a tenth of the information the CEO is working on. And the CEO was a smart guy, that's why we all invested in him. And I eventually just, you know, told him so in the board meeting, which is again, just me making friends and influencing people. But, you know, luckily for me, the investing partner, his partner, just started to laugh.

Jerry Neumann:Because I think we all felt the same thing, which is like, okay, you know. And the paradox was, this guy was incredibly valuable. He helped the founder more than any of us, when we weren't in board meetings. He he would go and actually meet with customers with the with the with the founder and help close them. I mean, he was great.

Jerry Neumann:And I think once he kinda settled down, he's like, alright. The CEO is running this company, and I'm here to help him succeed. Because if he succeeds, I succeed, then he was the the best board member ever.

Seth Winterroth:One of the biggest lessons in my career has been taught to me by the two of you, which is, you know, outlier companies get created from individuals, outlier individuals that are making outlier unique decisions on how they want their company to run and operate every single day. And if you have a boardroom that's filled with people that are kind of defaulting to the average of what they've seen drive success previously, you're by nature not indexing towards outlier decisions that create unique company culture and unique architectural decisions and unique hiring processes and unique comp

Bryan Cantrill:structure and all that kind of stuff.

Seth Winterroth:You see where I'm going here? Comp structure. And that but the thing the thing that matters most is results. Like, you guys are getting phenomenal results. And so like, is, you know, you you you do it your way.

Seth Winterroth:You play the game in the way you want to and you succeed at a level that you're succeeding. You should be empowered to go continue to be outlier in the way you think about designing and affecting your company's day to day operations from the ground up.

Bryan Cantrill:Yeah. Interesting and appreciate that. Appreciate you supporting our various idiosyncrasies. Because we do get this occasionally where you're like, you because, like, we do a lot of things differently. It's like, think about this.

Bryan Cantrill:Like, well, know, they're they're thoughtful about it. Like, they they take this you take this stuff apart, and they're willing to see what we see. And, you know, they they're willing to dig in. They're they they don't I

Steve Tuck:think I think that's the appreciation. It's not like a complicit, like, sure. Just do

Bryan Cantrill:Do whatever Do whatever you do. Do whatever dumb thing you Right.

Steve Tuck:Or saying, sorry. Like, this this does not pattern match on where we have seen even other successful companies do certain things a certain way, but actually digging in. Like, okay. What how'd you land here? Why what was what, you know, what was this informed by?

Steve Tuck:What have you seen that's worked really well about this? What have been the challenges? And inevitably, like, how do you scale? And and being being there and being thoughtful about it and collaborative about it has been has been terrific.

Seth Winterroth:But I think, like, what's true about you guys is is and the company is your ambitions have been clear from day one.

Bryan Cantrill:They really have.

Jerry Neumann:Love your

Seth Winterroth:love your customers and change computing forever. Like inherent within those values is desire to like shake the world on its axis and you're getting those results. So, the the first principles thinking that informs the way you does you get to a conclusion around everything big and small in the company is is wonderful, but the results, you know, you guys are getting tremendous results.

Bryan Cantrill:Yeah. Jerry, you did have I think he's when you were here last time, you were saying that like, look, like the company is gonna completely change with what you're doing. Like that's not like, you know and I actually we might be the rare exception to that. If you look at our original pitch, it's like we are actually we are doing what we kind of set out to go do. But I I but I also appreciate that we're idiosyncratic in that regard.

Bryan Cantrill:I think that is much more common cases that you end up with a lot more pivots on the way. And we've actually had plenty of like, I would say pivots below the waterline of the pitch deck. Like what we're doing is headline the same, but we've had lots and lots of ways in which the the actual manifestation of this has been surprising.

Jerry Neumann:Yeah. No. I I invested in a business once that was that actually did what they said they were gonna do when I met them. It was like in like 1998 or something. I just, you know, you don't see it very often.

Jerry Neumann:And that's okay, right? That's what you're trying to do. I mean, if you know what has to be done before you do it, then everybody else knows too. I mean, then it's just common knowledge. So either you're the best in the world at something, and you're the one who's going to win, or and you're gonna have a lot of competition, or you're out there and you're you're actually exploring what, you know, exploring what might work by trying things.

Jerry Neumann:Right? And that's what most founders do. So I there's no problem with that. That's how it's supposed to work.

Adam Leventhal:Right.

Bryan Cantrill:Adam, what's your your perspective on all this? Because I mean, the the you've I mean, you've been through all of this. And what what what was your takeaway on the book for some and what what what are your thoughts?

Adam Leventhal:Yeah. So I I founded a company. And and before that, I was I I remember sitting on a board at at the company. Before that, I was invited in as I became CTO. And I remember how how weird it was to sort of be brought into this.

Adam Leventhal:And I think that one of the things I I took away from Liz and Jerry's book is just sort of further like, knowing what normal is is very hard for for founders or folks who have only gotten an end of one or two or three to figure out, like, what is normal and what's aberrant? So for example, in my I remember in the first board meeting, the CEO took me and the this the the new VP of engineering and really told us what to say. And there's this whole Potempkins meeting. And I thought that was how it was. I thought that's how it was supposed to be.

Adam Leventhal:So I remember thinking back to this, reading reading their book, just thinking how useful it it would be to have the perspective of like, no. This isn't normal. This is weird. Like, this is a weird thing. You're being a weird act that that you all are performing for this board.

Adam Leventhal:Although in his defense, the board was pretty terrible and definitely did not read the materials beforehand and was going to get their pound of flesh one way or the other, whether it was useful or not. So

Bryan Cantrill:Yeah. So, Liz, what has been the reaction to the book? I I I have founders had the kind of reaction that Adam has had like, oh, wow. Thanks. Like, this is like, I didn't know that my board meetings were unusual or I'm glad that someone else has had this experience.

Liz Zalman:They they were I'll actually just say to what Adam just said, which is that is exactly how I used to prep my executives for board meetings in my company. I wanted them to say exactly what I wanted them to say and exactly the words I wanted them to say that and not a word more because it was going to get them and then me into trouble. So I I don't know how unusual that that setup was. But

Adam Leventhal:Well, think, Liz, I would I would just say, I think when the it verges on not being particularly true was the parts that I think were were potentially more aberrant, not not so much the the the the, like, let let's stay on the message, but when the message and reality are a little bit more divergent.

Bryan Cantrill:It was the lies, The not the

Adam Leventhal:lies. Right.

Liz Zalman:Fair enough. Mine were performative at best.

Jerry Neumann:Fair enough.

Bryan Cantrill:There we go.

Liz Zalman:I think the reception has been great. I I The reception that I've received, I'm guessing is different than Jerry's. Founders have reached out to me through email and on LinkedIn just saying thank you, thank you, thank you. And also asking for real operational advice specifically during fundraisers and term sheet negotiation with what to do in this particular situation. And believe it or not most of the questions actually veer around we need money.

Liz Zalman:We're desperate. We have a term sheet from somebody that we hate. What should we do? That's the top

Jerry Neumann:question I get asked.

Adam Leventhal:Brutal. And what and what do you I mean, that that that is very familiar and, like, brutal. And what do you tell them?

Liz Zalman:I tell them that there are always more fish in the sea and that as a founder, their job is to find a way forward and to survive for another day. So I try to tell them to avoid that money whenever possible. But I actually, let me ask Jerry, because I haven't asked him this in a while, Jerry, what has the reception you've gotten been lately?

Jerry Neumann:Well, I think on the back of the book, we actually blurbed a VC that I know who's somebody I've co invested with, and I asked if he would we were looking for somebody to write a forward next to Sandy Lerner's because she's a founder and her forward was pretty anti VC, which is understandable given And her so I wanted a VC to write one as well, in the spirit of the book, like a back and forth, right? I could not find anybody who would write one. And one VC who I knew really well, and I think he was well intentioned, said, You should cut yourself loose from this book and from Liz. This is not going to be good for your career. Which, you know, I was like, What career?

Jerry Neumann:I don't care. I'm an angel investor, I don't have a career. You know, so but that was you know, nobody wanted to talk about it. Nobody no VC would agree to it. I I just think, for me, that has changed a bit since then, I should to answer Liz's question.

Jerry Neumann:I I think the the VCs who are a little more introspective and like, you know, let's actually listen to what a founder has to say when they're not here trying to take trying to get money from us, because that can inform, you know, how we think about people that we're that aren't asking us for money, right? When people ask you for money, they're going be nice to you. Let's listen to what somebody says when they're not asking us for money, and then see what we can do better. And I think the good VCs have done that. For the most part, I think most VCs have been dismissive of the book at best.

Jerry Neumann:But yeah, so I don't know. Liz, what would

Liz Zalman:I was just gonna say, Jerry and I, because we were getting so many questions early on, we actually created a a chatbot. So if you go to founderversusinvestor.com, you can chat with the book, and you can ask me and Jerry questions. That's crazy. Author of trained on our individual voices, and we will we will answer you to the best of your ability.

Steve Tuck:Listeners pouring over there right now.

Jerry Neumann:Yeah. Yeah. This is an any questions organized in trouble. 47.

Bryan Cantrill:Yeah. That's I get it. I mean, Jerry, this is a

Steve Tuck:little surprising. I mean, maybe maybe I shouldn't be surprised, but I would just imagine that VCs would be excited about being able to look behind the curtain a little bit. That No. Around some of these conflicting concerns. Because I I think a lot of the book is pragmatic.

Steve Tuck:It's it's not taking I mean, again, as I as I listened to the Invest Like The Best podcast, I felt because it was my first time arriving at the content and this sort of dynamic of the two of you debating these things, and it felt a little bit more, contentious. But the book is like just laying out, you know, okay, well, why does VC exist? And what are the incentive structures in place? Namely, make your LPs, you know, have have as high returns as possible for the LPs. And to do that, you have to pick companies that are gonna take big swings in big markets and and be successful, and you're gonna have few successes.

Steve Tuck:And then, yes, different dynamics between a single partner and, you know, a partnership. And then from a founder perspective, you know, all of the you have an idea, then you have a presentation of an idea, and you have a narrative, and you gotta get by with that until you have enough capital to get enough team and traction to prove with customers you can build a thing, and then you can scale the thing. And that a lot of times these are in in in lined up the same way, and sometimes they're they can contradict each other. But I just I felt like it gave a great opportunity for both founder and investor to try on the other person's shoes and therefore be better informed the next time they are either investing or raising capital.

Jerry Neumann:Sure. But as a VC, what's your main advantage in the negotiation with a founder? Isn't it the fact that you actually know what's happening and they don't? Yep. I mean, seriously, like, mean, this is true of any, you know, anybody who's a middleman, right?

Jerry Neumann:And you traffic in information. Can go into a people company, they're like, Hey, you know, I want you to invest in my company, and what do they know about what valuations are? They know what they've read in the press, which are all completely distorted, or they know if they know other founders what the other founders tell them. I know an awful lot, right? I mean, I see a lot of deals.

Jerry Neumann:I talk to a lot of VCs. They tell me about all the deals they see. I have a pretty complete feel for in my sectors what valuations should be. If founders come in and ask me for a valuation that's too high, I say no. If they ask me for a valuation that's too low, well, okay.

Jerry Neumann:You know, I mean, not too low because if it's too low, then it doesn't work either. But you know, this is it's it's asymmetric information. So I I think part of it was that, not in valuation terms, but in terms of everything else. They would like the founders to rely on their

Seth Winterroth:who thinks you guys gave away the keys to the kingdom, and now all these founders are gonna be in a better position to, you know, I don't know, is is missing the forest through the trees.

Jerry Neumann:Well, totally. I mean, I don't think any of those VCs actually read the book. But it That's a good thing.

Bryan Cantrill:By the way,

Jerry Neumann:even the number of VCs who read

Seth Winterroth:more materials, I think that's probably definitely true.

Jerry Neumann:Yeah. Right. Yeah. But as an example, like, there were, like, three VCs who when they were, like, new and they started podcasts, and they said, hey. You've been doing this a long time.

Jerry Neumann:People know your name. Will you come on my podcast? It'll boost my boost my listeners and etcetera. I was like, yeah. You know, I I would love to do that.